Don’t Let Your Token Drown: How to Bootstrap Liquidity before your TGE

Introduction

Launching a token is one of the most pivotal moments in the lifecycle of any blockchain project. The Token Generation Event (TGE) is not just a milestone for your community—it’s the moment when your project’s vision, tokenomics, and execution collide in a live marketplace. A successful launch can set the tone for years to come, while a poorly managed one can create lasting damage to your token’s credibility.

At the center of this critical juncture lies a single concept: liquidity. Liquidity is what allows investors to build and exit positions with confidence. It ensures that price discovery reflects fair value rather than speculation driven by thin order books. Without it, even the strongest fundamentals can be overshadowed by volatile charts and shaken investor sentiment.

This is why understanding and engaging with market makers (MMs) is essential. Market makers are not altruistic participants; they are profit-motivated institutions that provide liquidity only when the incentives align. Structuring those incentives correctly can mean the difference between a sustainable, efficient market and one that quickly unravels.

In this blog, we’ll break down best practices for engaging market makers before your TGE, structured into three key parts:

- Covering the Basics – What liquidity is, why it matters, and why it doesn’t naturally exist for your token.

- Practical Approaches to Bootstrapping Liquidity – A deep dive into the two dominant MM engagement models (retainer + working capital vs. loan + call option), including examples, trade-offs, and risks.

- Structuring Favorable Engagements – How to mitigate risks, align incentives, and set up win-win relationships with market makers through smart structuring and RFQ processes.

Our goal is to equip founders and token teams with the clarity they need to navigate one of the most misunderstood yet impactful parts of going to market: liquidity and market making.

Part 1: Covering the Basics

What is liquidity and why is it important?

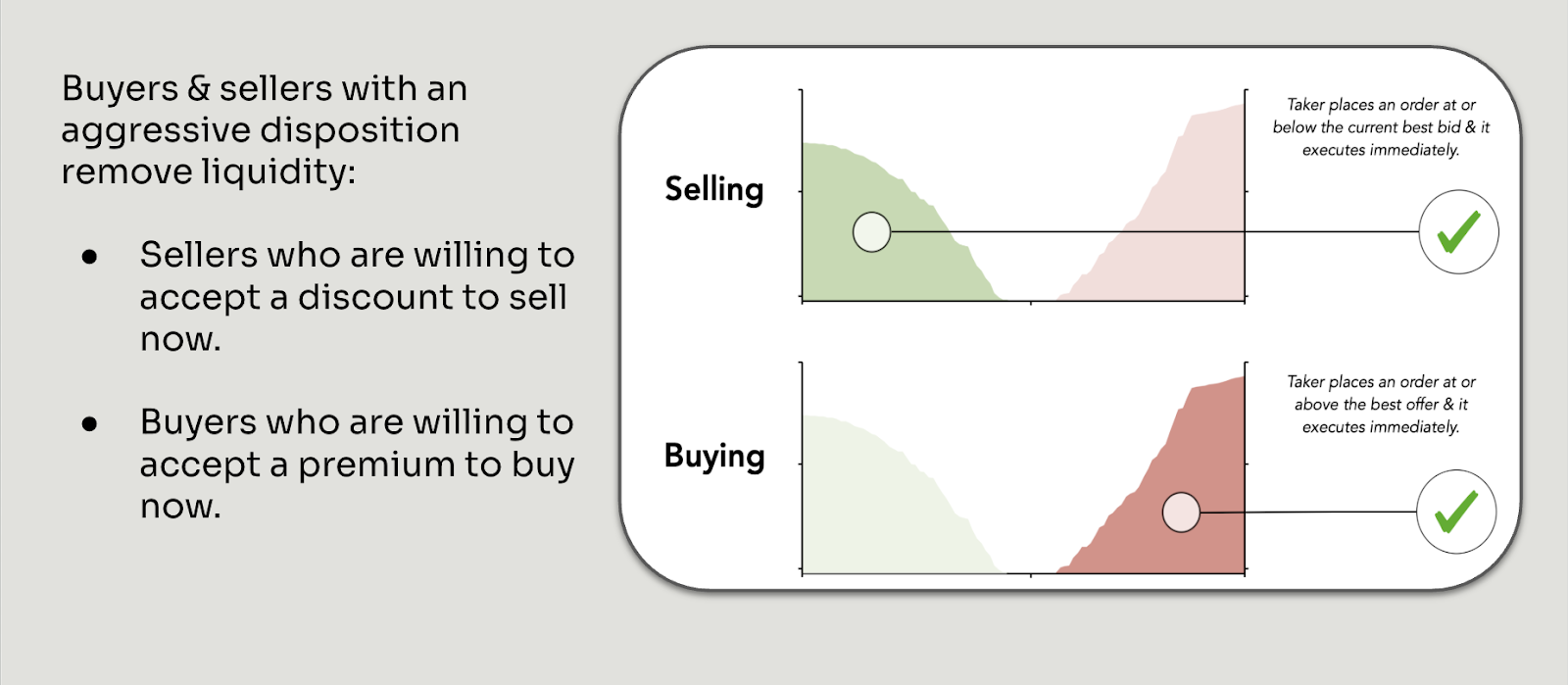

Liquidity is often talked about but rarely defined with precision. At its core, liquidity is the presence of patient buyers and sellers in a market. Patient sellers are willing to wait for a premium, and patient buyers are willing to wait for a discount. Their willingness to “sit on the book” is what creates depth.

This depth allows aggressive traders—those who want to transact immediately—to buy or sell without moving the price too dramatically. In other words, liquidity empowers immediacy. A healthy market is one where participants can trade what they want, when they want, with minimal transaction costs.

For a newly listed token, this is critical. Liquidity is the foundation that underpins investor confidence, fair price discovery, and sustainable growth.

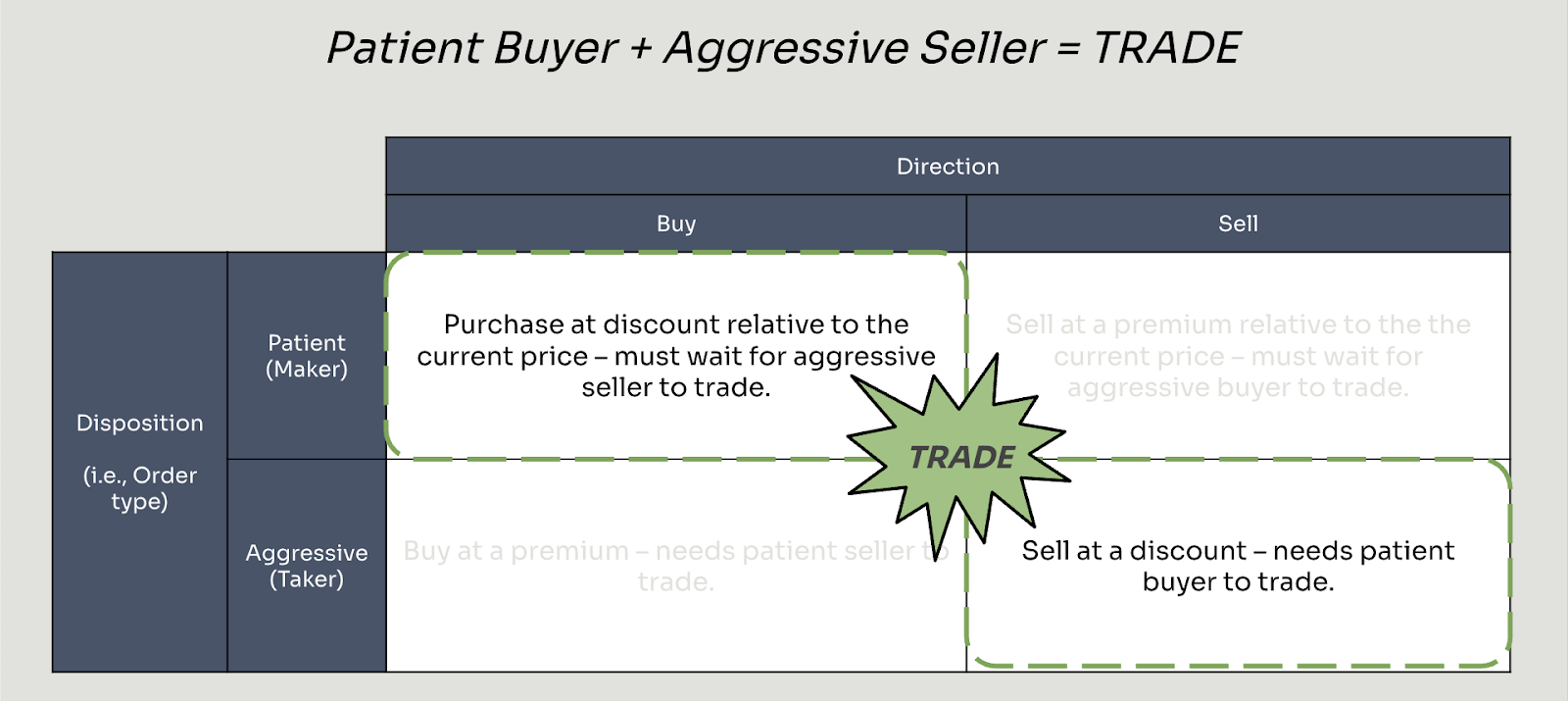

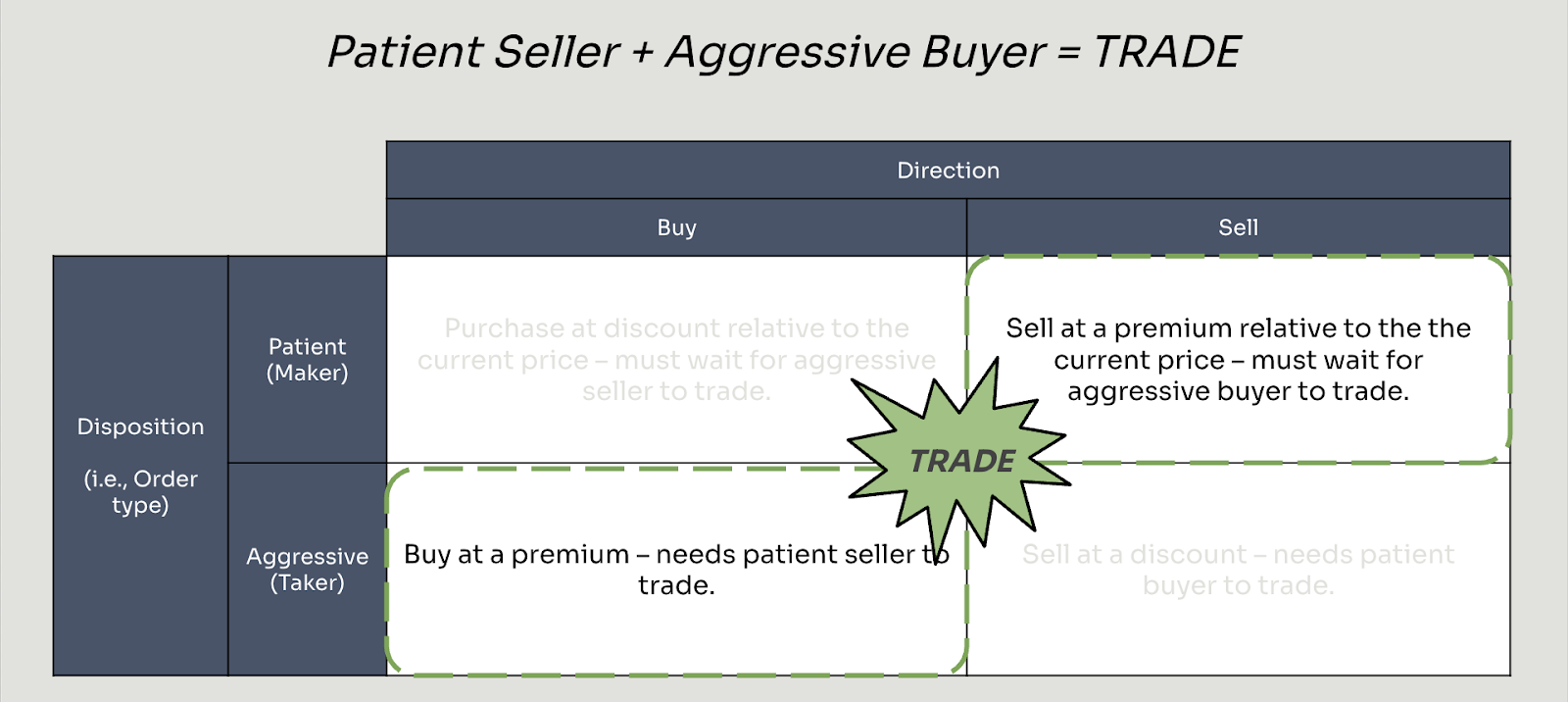

All trades are a function of direction and disposition

Every trade requires two things:

- Direction – Are you buying or selling?

- Disposition – Are you patient (a maker) or aggressive (a taker)?

A patient buyer pairs with an aggressive seller. A patient seller pairs with an aggressive buyer. It takes two to tango. Without patient participants providing liquidity, aggressive traders cannot execute, and markets quickly become dysfunctional.

Benefits of liquidity

Liquidity provides several benefits that extend beyond smoother trading:

- Investor confidence – Institutions and retail alike are reluctant to build positions if they fear they cannot exit without moving the market. Deep liquidity signals stability.

- Higher trading volume – Tighter spreads and deeper books encourage more activity, which in turn attracts more participants.

- Efficient price discovery – A liquid market ensures that price reflects collective market sentiment, not the last aggressive trade.

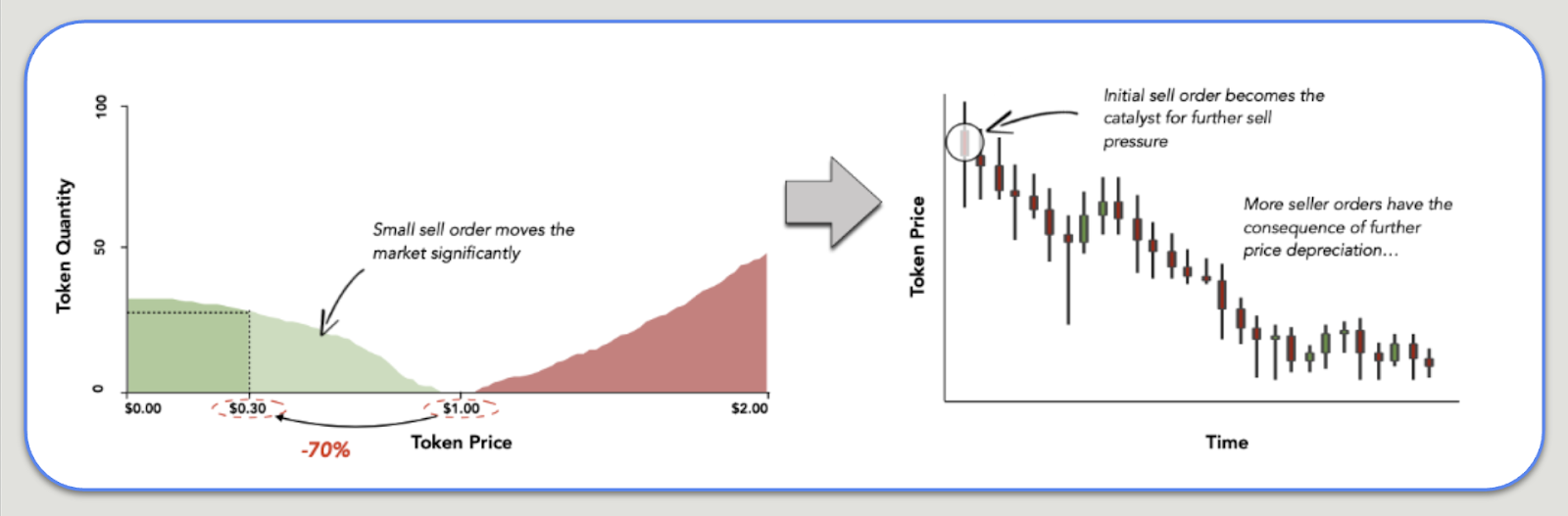

The risks of poor liquidity

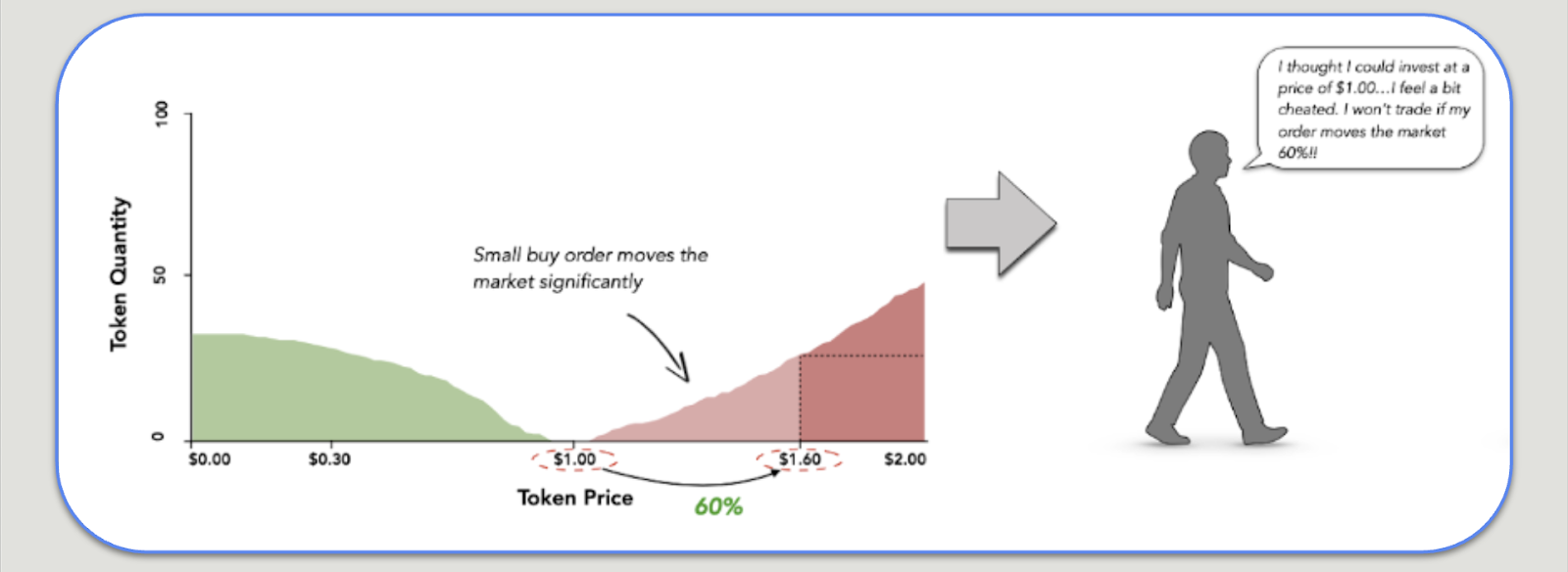

The flip side is stark. Shallow liquidity means that even small trades can create disproportionate price moves. A modest sell order can spark panic selling, as investors interpret price declines as deteriorating fundamentals.

Conversely, shallow offer-side liquidity can scare off institutional buyers who cannot build meaningful positions without paying a massive premium.

The result: volatile charts, disillusioned communities, and reputational damage at the most sensitive point in your project’s lifecycle.

Why do people provide liquidity?

A common misconception is that liquidity is a “public good.” While it benefits all participants, liquidity providers are not altruists—they are profit-motivated.

- On order-book exchanges (CLOBs), market makers profit by capturing the spread: buying low and selling high on the same book.

- On AMMs, liquidity providers earn trading fees and often yield-farming rewards.

For your token, market makers will only engage if the expected value (EV) of providing liquidity is positive compared to other opportunities they have.

Why doesn’t liquidity exist organically for my token?

For most pre-TGE projects, liquidity does not materialize on its own. This is because the EV for a market maker to provide liquidity is often:

- Negative (unprofitable),

- Uncertain or unpredictable, or

- Lower than alternatives like BTC, ETH, or SOL, where volumes and opportunities are abundant.

Challenges include:

- Fair value uncertainty – Without a track record or fundamentals, it’s difficult to price a new token.

- Low volume – Few trades mean fewer opportunities to capture spreads or fees.

- Capital intensity – Market makers must commit both stablecoins (to buy) and tokens (to sell). Reallocating capital from majors into a new token is usually unattractive without additional incentives.

This is why projects must actively incentivize specialized market makers—structuring agreements so that providing liquidity becomes worthwhile.

Part 2: Practical Approaches to Bootstrapping Liquidity

Liquidity doesn’t appear for your token organically—you need to incentivize specialized institutions to provide it. Over the past several years, two dominant engagement models have emerged for blockchain projects:

- Retainer + Working Capital

- Loan + Call Option

Both models seek to make the expected value (EV) of providing liquidity positive for market makers, despite the risks of trading your newly launched token. Let’s break them down.

Retainer + Working Capital Model

Overview:

- Typically used by small to mid-sized trading desks that act as “in-house” service providers.

- They don’t usually trade their own balance sheet; instead, they trade using the capital (tokens + stablecoins) that your project provides.

- Their revenue comes from a combination of monthly retainers, onboarding fees, and sometimes profit shares if they grow your inventory.

Example:

The Good:

- Operates as an extension of your team.

- Strong alignment if profit share is included—market makers are motivated to grow NAV.

- Effective “opening specialists,” smoothing price action at launch.

The Bad:

- Requires significant stablecoin allocation, which can be prohibitive.

- Fees (retainer + onboarding) add to operating costs.

- Many desks run hundreds of clients simultaneously, limiting discretionary support.

The Ugly (“Catch a Falling Knife”):

- If prices drop, these desks often step in aggressively to buy and stabilize.

- If the market continues down, they may deplete stablecoins at poor levels.

- End result: NAV skewed heavily toward tokens, leaving projects frustrated that scarce stablecoins were converted into assets they already had plenty of.

Loan + Call Option Model

Overview:

- Common among large, global trading firms (e.g., Wintermute, GSR, Flow Traders).

- They use their own balance sheet and proprietary trading strategies.

- Projects provide token loans with embedded European-style call options (the right, but not the obligation, to repay in stablecoins at expiry).

Example:

The Good:

- No upfront fees or stablecoin allocation required from the project.

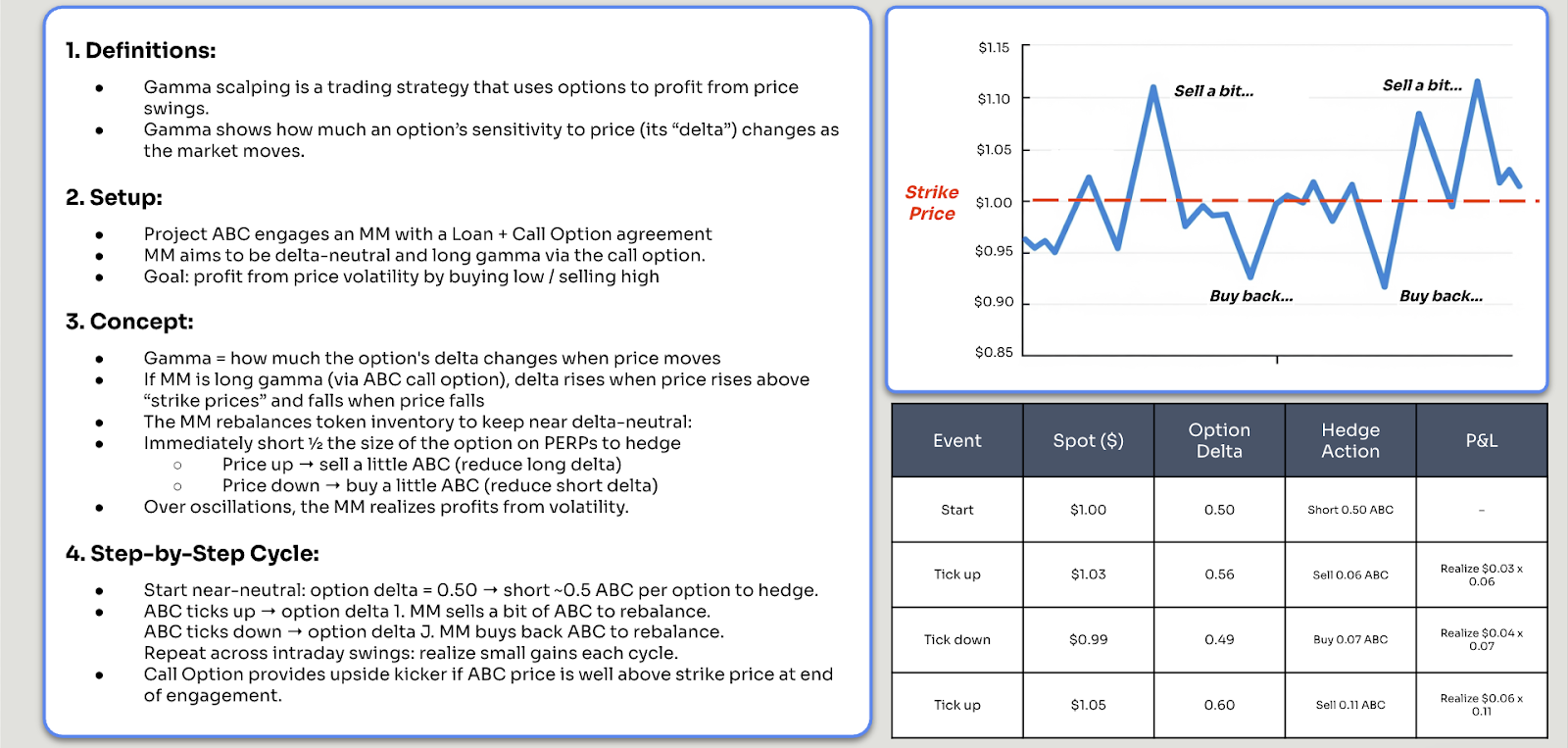

- Potential for deep liquidity near strike prices, especially if MMs engage in gamma scalping (hedging strategies that profit from volatility).

- Stronger long-term support if options are in the money.

The Bad:

- Gamma scalping only works if there is a liquid perps market and volatility around strike levels. If the token trends down, MMs stop scalping.

- Projects have little control—these desks act with full discretion, potentially prioritizing their profit over stability.

The Ugly (“Parasitic Strategy”):

- Many MMs anticipate “down-only” trajectories.

- They may allow a euphoric post-TGE pop, then aggressively sell into retail demand.

- This drives cascading sell pressure, weakens community sentiment, and leaves the MM in position to repurchase tokens cheaply later.

- Often, they never exercise the options—meaning no cash inflow for the project.

Comparing the Two Models

- Retainer + Working Capital → Risk is borne by your stablecoin treasury. Expensive but stabilizing if structured correctly.

- Loan + Call Option → Risk is borne by your token price. Low upfront costs but potentially parasitic if not carefully structured.

Summary of “The Good, Bad, and Ugly”

Gamma Scalping: A Double-Edged Sword

Gamma scalping deserves special mention. It is the process of buying low and selling high around strike prices to harvest volatility.

- Benefit for projects: Tighter spreads, smoother price discovery, deeper books.

- Benefit for MMs: Direction-agnostic profit opportunities + upside kicker if options end up in the money.

- Risk: If the market trends “down only,” gamma scalping stops. The MM may instead short aggressively, adding sell pressure.

Key Takeaways

- Both models have trade-offs. Retainer protects price but drains stables; Loan + Call saves treasury but risks parasitism.

- Align incentives. Always structure agreements so MMs can profit responsibly (profit share for retainers; achievable strike prices for options).

- Monitor performance. Don’t just trust contracts—track liquidity depth, spreads, and execution quality in real time.

Part 3: Structuring Favorable Engagements with Market Makers

Designing liquidity support isn’t just about choosing between retainer and loan models. The real work is in structuring agreements that align incentives, mitigate risks, and set your token up for long-term success.

The Forgd RFQ Process

Forgd has developed a competitive Request for Quote (RFQ) process to help projects engage with MMs transparently:

- Submit preferences – Projects indicate their priorities (e.g., cost control, deeper liquidity, long-term support).

- Market makers bid – Multiple desks submit proposals, adjusting terms based on competitive tension.

- Data-driven review – Forgd benchmarks offers against historical trading performance to identify credible partners.

- Ongoing monitoring – Once engaged, projects track MM activity via dashboards that measure spreads, depth, and adherence to KPIs.

This competitive process shifts leverage back to projects, ensuring they’re not at the mercy of opaque bilateral deals.

Risk Mitigation Strategies

For Retainer + Working Capital

- Profit share is key. Without it, MMs behave like service providers rather than asset managers. A share of NAV growth keeps them aligned with your success.

- Guardrails around NAV. Ensure profit share is based on realized stablecoin gains, not inflated mark-to-market values.

For Loan + Call Option

- Minimize token allocations. Only provide what’s absolutely necessary to provision liquidity—never over-allocate.

- Diversify strike prices. Spread tranches across multiple timeframes (e.g., TGE, 3 months, 6 months). This prevents MMs from shorting 100% of inventory early.

- Avoid clustered strikes. If all strikes are set around the first week, MMs have a free hedge and little incentive to support long-term.

The Ideal Setup

There’s no “one-size-fits-all,” but Forgd strongly encourages projects to select one business model and stick with it for all Market Maker engagements.

- Primary MM (Retainer + Working Capital) – Acts as your stabilizer, funded with tokens + stables, aligned by profit share. Provides orderly books and guards against egregious volatility.

- Secondary MMs (Loan + Call Option) – Larger desks with scalable infrastructure. Incentivized with realistic strike prices spread over months, ensuring depth across price bands.

Final Thoughts on Structuring

At the end of the day, market makers are profit-motivated counterparties, not white knights. But when engaged thoughtfully, they can provide the depth, stability, and credibility your token needs in its most fragile stage.

By using a structured RFQ process, aligning incentives, and balancing engagement types, projects can transform market making from a risk into a strategic advantage.